By BILL BRANDON

The Rockefeller Brothers Fund made recent headlines with their announcement to divest fossil energy stocks. The ramifications may be more complicated than you think since there are two sides to the issue. One side is very simple; the other side is rather complex. Examples presently hitting the media are the first side of the issue and are social statements like the Rockefeller announcement. Such actions can eventually render a company a social pariah but have no economic effect on the company. Vox media had a recent post on this question that reveals the lack of economic impact associated with such a divestiture.

The other side of the issue is the question of divestment based upon a belief that fossil fuel companies will eventually end up with large ‘stranded assets’. Stranded assets are inventories (like known oil reserves) or equipment that are carried on the books but have no real or low value. This can result in an over evaluated company and would essentially be a bad investment. Companies are slow to write off such assets and almost never discuss risks or probability of these assets losing value in their shareholder reports.

Fracked Oil and Gas

Since proven reserves are based on viability at a given cost with a given technology, price and production costs directly relate to the value of these assets for the short term. This is particularly true of fracked oil and gas, the ‘future’ of our petroleum reserves. With conventional oil or gas, after initial discovery and drilling costs, production costs are very low. With fracking there is a continuous need for water, sand, chemicals and energy to extract the oil and gas. The recent 20% decline in crude oil energy prices has caused a few wells to be shut down and a majority will not be profitable if prices fall below $75 per barrel. Many gas wells are presently capped because natural gas prices are too low to justify production.

In the long term, uncertainty based on potential regulations as noted by ICF represents financial risk. These risks are based in the World Carbon Budget. Only one third of known fossil reserves can be burned between now and 2050 if we’re going to remain below the allowable CO2 emissions necessary to limit global temperature rise and avoid significant climate change. To avoid disruptive climate change, some have proposed a strict CO2 emission regulations or a carbon tax that will change the existing business model, lower asset value, and strand assets.

” The recent 20% decline in crude oil energy prices has caused a few wells to be shut down and a majority will not be profitable if prices fall below $75 per barrel. many gas wells are presently capped because natural gas prices are too low to justify production.”

Fossil Fuel Investments

Contemporary society cannot exist without investment in energy, period. We first need to look at the question of why fossil fuel investments have been important to institutions. The direct answer is that they have been a good investment. They provide a stable and relatively high rate of return, and more importantly, they have been highly liquid. If an institution is going to divest their fossil fuel stocks, the important question is where are they going to invest that money and will the investing institutions get a similar return on investment?

Student leaders at Stanford University convinced their institution to divest suggesting that this money could be invested in campus improvements to lower the overall carbon footprint of the campus and to lower operating costs through efficiency. But how does that relate to the investments it would replace? How does it pay for professors’ retirement or pay checks or student scholarships? Returns from endowment investments are needed as a cash flow to meet these intended needs.

If institutions do not return that money as investments in some form of alternative, sustainable energy or materials, their effort will be entirely symbolic. And here is the difficulty for those institutions – no alternative energy stock will meet the same ‘quality’ as a stock of an established fossil fuel company who enjoys imbedded tax advantages and other favorable economic treatment such as monopolistic market access or Master Limited Partnership. These types of investment formats or accounting rules allow reserves to be carried as assets on balance sheets or avoid corporate taxes.

Low Carbon Economy

Alternative energy can’t carry the sun or wind as an asset on their balance sheet nor can biofuels carry future crops as ‘reserves’. This unequal accounting rule distorts company values and makes it harder for alternatives to raise money. Moving to a low carbon economy will require a lot of investment so we must determine how that money can be accessed. Parenthetically, some think that China is in a better place to move to a low carbon economy than western nations because they are better able to direct investments. This is due to their lack of legacy of investments in fossil fuels. Therefore, investigation and innovation of mechanisms that make low carbon investments an appropriate investment for institutions is needed.

It is also important to recognize that fossil fuels are not equally creating greenhouse gases (GHG) for a variety of reasons. Centralized utility electrical generation using natural gas releases fewer GHGs than coal because gas is both a lower carbon molecule and combined cycle gas generators can reach significantly higher efficiency rates. Adding combined heat and power (CHP) improves both. (It should be noted that fugitive methane emissions from production and transmission can add to GHG emissions. The significance of these emissions and the ability to reduce them is presently a point of debate). Extracting oil from tar sands is a high carbon enterprise for a variety of reasons. On the other hand, extracting oil from depleted oil fields using ‘waste’ CO2 from a power generator results in a significant reduction in overall GHG emissions.

Here’s an example where the process is working:

NRG Energy, a publicly traded corporation, is a relatively progressive energy company. They are building the first CO2 capture system and distribution pipe line for Enhanced Oil Recovery (EOR) from south of Houston to the Port Lavaca area for the Petra Nova project. Even with EOR, this field would be ‘played out’ in about 12 years. With CO2 pipeline structure in place and plenty of Gulf salt water easily available, this field could continue to produce algae derived biofuels through technologies now being commercialized. These volumes would be about one half the volume of the oil field production rates. Such a sequential strategy could extend the asset value of these oil field and infrastructure almost indefinitely.

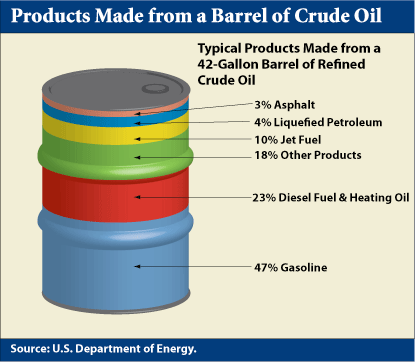

I have seen it suggested that we should reserve our petroleum for making chemicals and products. This is a ridiculous proposition on two levels. First, carbon is fungible; sequestering one ton of fossil carbon while releasing one ton of renewable carbon is just the same as sequestering one ton of renewable carbon while releasing one ton of fossil carbon. To reserve high margin chemicals for petroleum while expecting renewables to emerge only as low margin fuels makes no economic sense. Twenty percent of a barrel of oil goes to the chemical market, which brings in 50% of the industries end product revenues. The remaining 80% goes to low margin fuels and brings in other 50% of revenues. As bio-chemicals capture market share from petro-chemicals, it will either put a downward price pressure on crude oil prices and consequently stranding assets or more likely, an upward pressure on fuel prices making them less competitive compared to alternatives and consequently stranding assets. big oil is more vulnerable to competition in chemicals than fuels.

There is opportunity for corporations to evolve within the traditional energy industry. Institutional investment in selected ‘traditional’ companies, followed by shareholder pressure to evolve rapidly toward a low carbon economy, can be a successful investment strategy to develop a low carbon economy.

The pressure on institutions should be to divest of fossil fuel companies only after the institution applies pressure on the corporation for greater transparency from to risks and mitigation strategies. Capital needs to flow to companies that are working towards true mitigation and adaption strategies for climate change. Investment strategies are not just in or out. While divestiture from the most ridged companies that cannot or will not change may be justified, but there remains the problem of finding appropriate investment structures for emerging technologies. Institutional investors need to help fill that gap by actively participating in developing innovative investment structures that are consistent with their investment needs.

Recommend Solution:

What are your recommendations on how to transition to a low carbon economy for developing new investment strategies?